Thursday, 10. June 2021

The company car market is predicted to grow significantly after new research reported a three-fold increase in drivers wanting to source their next vehicle through their employer.

The findings, from the OC&C Speedo meter ‘Battery Late Than Never’ report, also suggest that Covid-19 has helped cement the importance of a car, despite people driving less.

More than two-in-five drivers (42%) said the pandemic has increased their belief that a car is essential. It is not just drivers who see the car as essential either – the number of non-drivers who expect to own in the future has risen by 21% in the UK.

The global report was published last week and is a follow-up to a 2019 study. It tracks how trends in consumer attitudes and behaviours toward vehicles and their mobility needs have changed.

Looking at UK-specific data, it shows that just 2% of consumers expected to source their next car through their employer in 2019, but, three years later, that has risen three-fold to 6% – a 200% uplift.

COMPANY CAR MARKET

It is a positive outlook for a sector which has been in decline for the past few years. The most recent figures, published by HMRC in September 2020, showed that the number of people paying company car tax had again fallen substantially, with HMRC reporting 30,000 fewer people receiving the benefit.

The benefit-in-kind (BIK) statistics, published by HMRC, showed there were 870,000 company car drivers in 2018-19 – a massive 30,000 year-on-year decline.

The figures suggested that the number of employees receiving the benefit had fallen by some 90,000 in the past five years, from 960,000 in 2015/16.

The introduction of a new zero percentage tax rate for a pure electric company car in April 2020, along with lower rates for hybrids, however, has led many to predict a brighter future for the benefit.

The latest new car registration figures from the Society of Motor Manufacturers and Traders (SMMT) highlight the relative strength of the sector.

Almost 80,000 new company cars were registered to fleet and business in April as the market continued to show signs of recovery.

Year-to-date, 318,991 new cars have been registered to fleet and business compared to the 259,017 units registered during the same period last year, a 23% uplift.

Fleet and business registrations now account for 56% of the market, with 567,108 cars registered overall.

There were 141,583 new car registrations in April, with 79,648 new company cars registered to fleet and business.

In April 2020, at the start of the first lockdown, just 3,450 new company cars were registered.

APPETITE FOR EVs

OC&C says the proportion of drivers considering an electric vehicle (EV) is “unprecedented” and is likely to translate into a fast acceleration in EV adoption.

Globally, more than 50% of drivers considered a hybrid when they last changed their car, and more than 40% report they will consider a pure EV next time.

The UK leads the West in EVs in the survey, with 57% of UK drivers considering fully electric for their next vehicle versus 45% in Germany and the US.

In the UK, new BIK tax rates will be persuading some to make the switch to a plug-in car, but the OC&C study shows range and tech improvements (38%), concerns about the environment (39%), Government regulation changes (36%) and better availability of charge points (35%) are the main drivers for consumers.

The OC&C data reflects the experience of leasing companies, which have reported a growing number of company car drivers choosing an EV.

Tusker, for example, has a risk fleet of approximately 20,000 cars and, while just one-in-33 (3%) were pure electric in 2019, it has since increased to one-in-five (20%).

Half of the leasing company’s orders in 2020 were for pure electric cars. Hybrid vehicles, both plug-in and mild, accounted for 20% of its new vehicle orders, with petrol and diesel responsible for less than a third (30%).

In fact, zero-emissions-capable cars, including electric, hybrid and fuel cell models, now account for one-in-three of the available models in the UK, according to the SMMT.

BARRIERS TO ADOPTION

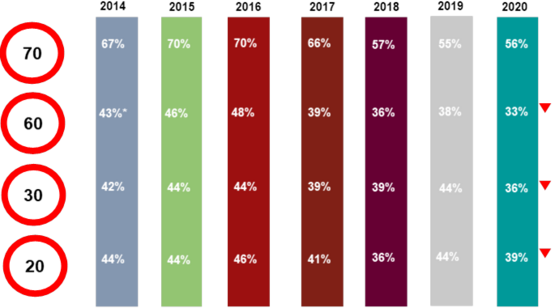

Barriers to adoption have shifted, with the OC&C report suggesting the percentage of people citing access to public charging infrastructure as an issue has fallen dramatically.

In 2019, it said that 64% of respondents in the UK saw it as a barrier to adoption; the latest study reports that it has fallen by 14 percentage points to half (50%).

An EV’s range, while still the number one concern, is also seen as less of a barrier, falling seven percentage points, from 62% to 55% over the same period.

Meanwhile, more drivers see vehicle cost as a barrier, with more than half of respondents (51%) highlighting it as issue, compared with 49% in 2019.

The cost of electricity saw the greatest swing, with more than a quarter of respondents (29%) citing it as a barrier compared with 19% in 2019 – a 10 percentage point uplift.

The Association of Fleet Professionals (AFP) says the lack of an effective national strategy for creating kerbside charging infrastructure is emerging as the biggest barrier to adoption of EVs by businesses.

OC&C’s study, however, suggests access to a charge point close to home or at the driver’s property is becoming less of an issue for UK consumers, with 39% citing it as issue in the most recent survey, compared with 44% in 2019.

The current Government approach to install kerbside charging means 75% of the cost is met by a national fund and 25% is paid by local authorities.

AFP chair Paul Hollick believes the strategy is not working. He said: “We have national fleets who are AFP members and want to go 100% EV as soon as possible. The stumbling block they face is that nationally, around four-out-of-10 people live in apartments or terraced houses and don’t have access to on-street parking.

“That means they are reliant on local authorities to install street charging facilities but, as you’d expect, the impetus and ability to do so varies massively from area to area.”

A kerbside charger costs around £2,500 to install, meaning local government needs to find £600 per unit. In the wake of the pandemic, Hollick says many simply don’t have the money, even if there is the will.

CAR CLUB POTENTIAL

Exclusive access to a car still remains vital to 82% of drivers, according to the OC&C report, with most expressing concerns around accessibility, storage and privacy as key to their reluctance to consider co-ownership or access models.

However, the importance of exclusivity is starting to wane for a forward-thinking minority, with 13% of UK drivers happy to consider mobility solutions as an alternative to having their own car, be it carsharing solutions, taxis or even short-term rental – a four percentage point increase on 2019.

OC&C says this reflects lower car usage in 2020 as a result of the pandemic, environmental and cost concerns, while the development of models such as Zip Car and Drover are also driving changes in attitude.

Consumers also continue to see a car as essential to travel, according to the report. The percentage of drivers who see a car as essential has remained stable between 80-90% since 2019.

This is true even among the young; Gen Y and Gen Z drivers still care about having cars and driving, it suggests. In fact, they have become more dependent on cars than they were. The percentage of 18-29-year-olds disagreeing that a car is essential has fallen from 11% to 5%. By Graham Hill thanks to Fleet News

Share My Blogs With Others:

These icons link to social bookmarking sites where readers can share and discover new web pages.