Tariffs on new cars and vans may have been avoided, but a lack of detail in the Brexit deal could still lead to disruption in the market, the remarketing industry has warned.

The Vehicle Remarketing Association (VRA) says that several key points surrounding the future of manufacturing and cross-border movement of vehicles remain vague or undefined.

Sam Watkins, chair at the VRA, said: “Let’s be clear on this – any deal is good news because it avoids the kind of tariffs that would’ve been attached to no deal. It is something that should be a huge cause for relief.

“However, the deal that we now have raises as many questions as it answers. It is generally being described as ‘thin’ and that is accurate in that there are several areas where there is very little detail for the motor industry or remarketing.

“We are probably entering into a process now where those points are going to be worked through, but it seems that some will be easier to resolve than others.”

As a result, Watkins expects disruption to car and van supply. “It’s quite difficult to separate the negative effects of the pandemic and Brexit but getting hold of a number of popular new models is almost certainly going to be tricky in 2021,” she said.

“For a motor industry that has finished last year around 30% down in new car sales compared to 2019, this is not good news, and there will be knock-on effects for the used sector that will persist into the medium term.”

Watkins believes that the reduced numbers of vehicles entering the market will mean that getting hold of the used stock will remain difficult. “The situation may even worsen compared to the last few months,” she said.

“However, if 2020 has underlined anything, it is that the used car sector is incredibly flexible and innovative, and that people will continue to want to buy despite substantial practical barriers in their way.”

She continued: “The threat of motor manufacturing in the UK potentially unravelling overnight has been removed, and this should mean that there is no immediate question mark over UK factories and supply chains.

“However, looking ahead, substantial costs have been added in terms of the new customs arrangements, and the regulatory background against which car makers operate is unclear in several important areas.

“Presumably, these will be clarified in the coming months and years but it does perpetuate an effect that has been present ever since the Brexit referendum – that it is difficult to make plans and for investment decisions to be finalised without all of the facts available. There remains a lot of uncertainty.”

Notably, there were special difficulties surrounding the rules of origin arrangements, claims Watkins, that could have implications for EV manufacturing in the UK. By Graham Hill thanks to Fleet News

Share My Blogs With Others:These icons link to social bookmarking sites where readers can share and discover new web pages.

Tesla expanded its UK dealer network to 25 sites during 2020 and plans further network growth in 2021.

It represents a U-turn on company founder Elon Musk’s 2019 declaration that Tesla would close all its showrooms in favour of an online-only sales model.

The latest strategy follows reports of Tesla’s value reaching a record £516 billion, making it worth more than Toyota, VW, Hyundai, GM and Ford combined.

Six new Tesla locations were opened across the UK in 2020, with new showrooms appearing in Newcastle, Winchester, Gatwick, Belfast, Birmingham and Chelmsford.

A new site in Glasgow is also poised to open this year.

The Californian car maker says it has boosted its aftersales operation significantly and now has 15 service locations across the country, with more than 300 service team members.

This has led to a 130% increase in available service appointments and a 60% reduction in waiting times for appointments, according to the brand.

Tesla says it can reduce the time vehicles need to be in a workshop using remote diagnosis and can perform a service four times faster than conventional garages, enabling it to operate with a smaller footprint.

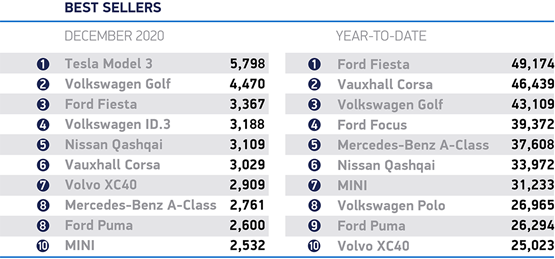

The brand achieved almost 25,000 registrations during the year, outperforming established brands such as Fiat, Mazda, Porsche and Suzuki.

Its Model 3 topped UK monthly sales charts twice during the year – once in April and then in December.

The vast majority of sales are the Tesla Model 3 – Tesla insiders suggest the Model 3 accounts for approximately 90% of UK Tesla sales YTD. That makes the Model 3 the UK’s best-selling battery electric vehicle (BEV), and the UK’s second best-selling compact executive model behind the BMW 3 Series.

Tesla’s UK Supercharger network also grew during 2020 with the addition of 180 new chargers in 20 locations, bringing the total to more than 600 chargers in 70 locations. By Graham Hill thanks to Fleet News

Share My Blogs With Others:These icons link to social bookmarking sites where readers can share and discover new web pages.

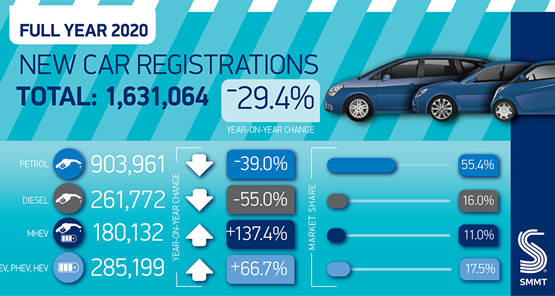

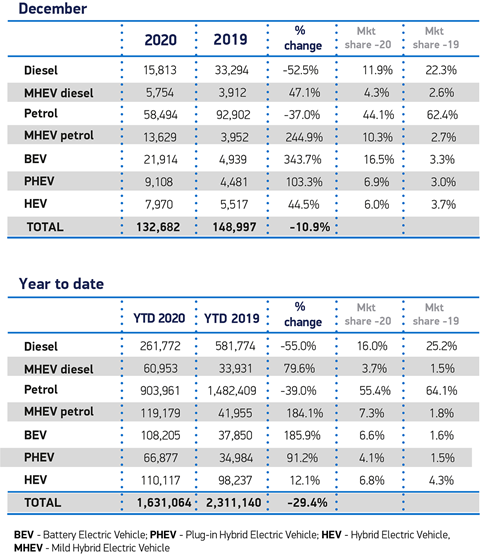

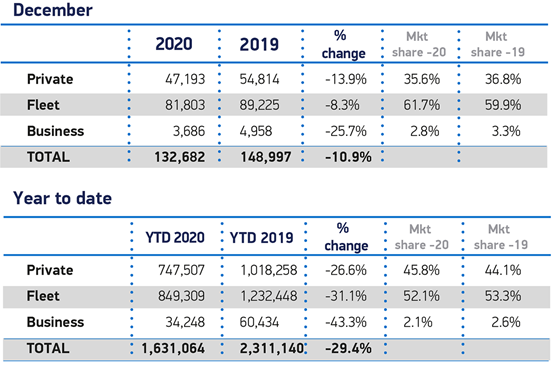

I don’t think that it would surprise anybody that new car registrations were drastically down in 2020 but the interesting statistic is the split of cars. Private registrations suffered the least with the larger fleets doing slightly better but the business registrations were down 43.3% (see chart below).

However, I would suggest that whilst these figures look dreadful many customers, both corporate and consumer extended lease contracts last year and those that had to change their cars decided to go down the used car route as there was a grave lack of new car stock available.

Here is the report and breakdown of the figures for 2020:

Fleet and business registrations fell by 32% in 2020, with 400,000 fewer company cars registered compared to 2019, but fleets were behind a massive increase in the uptake of electric vehicles (EVs).

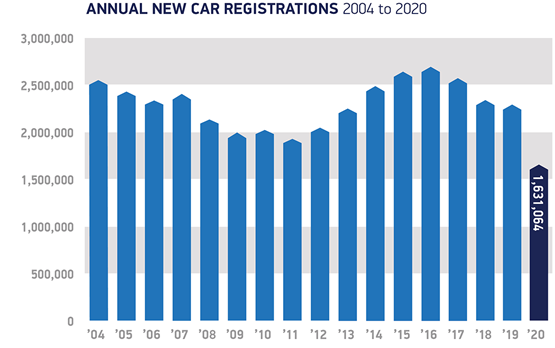

The new figures, published today by the Society of Motor Manufacturers and Traders (SMMT), show overall demand in the new car market fell to the lowest level since 1992.

They also reveal the continuing decline of diesel, with 55% fewer diesel cars registered in 2020 compared to 2019.

The SMMT sales figures show there were 883,557 cars registered to fleet and business during 2020, compared to almost 1.3 million vehicles the previous year.

However, the latest sales data also reveals that in December, fleet and business registrations were only 9% down compared to December 2019.

It suggests a recovering company car market, with 85,489 fleet and business registrations, equating to 64% market share.

Overall, the UK new car market fell by almost a third (29%) in 2020, with annual registrations dropping to 1,631,064 units.

Against a backdrop of Covid-19, the industry suffered a total turnover loss of some £20.4 billion, with private vehicle demand falling by 27% overall, amounting to a £1.9bn loss of VAT to the Exchequer, says the SMMT.

Mike Hawes, chief executive of the SMMT, says that 2020 will be seen as a “lost year” for automotive, with the sector under “pandemic-enforced shutdown” for much of the year and uncertainty over future trading conditions taking their toll.

However, he said: “With the rollout of vaccines and clarity over our new relationship with the EU, we must make 2021 a year of recovery.

“With manufacturers bringing record numbers of electrified vehicles to market over the coming months, we will work with Government to encourage drivers to make the switch, while promoting investment in our globally-renowned manufacturing base – recharging the market, industry and economy.”

Demand fell across all segments bar specialist sports, which grew by 7%, although Britain’s most popular class of car remained the supermini, retaining a 31% market share despite a 26% decline in registrations.

Meanwhile, although falling by a combined 33%, petrol and mild hybrid (MHEV) petrol cars made up 63% of registrations, while diesel and MHEV diesels, down 48%, comprised almost a fifth of the market.

Fleets adopt more electric vehicles

Battery and plug-in hybrid electric cars accounted for more than one in 10 registrations – up from around one in 30 in 2019.

Demand for battery electric vehicles (BEVs) grew by 186% to 108,205 units, while registrations of plug-in hybrids (PHEVs) rose 91% to 66,877.

Most of these registrations (68%) were for company cars. Gerry Keaney, chief executive of the British Vehicle Rental and Leasing Association (BVRLA), says that 2020 has been a “tipping point” for EV uptake and demonstrates what can be achieved when Government works closely with fleets to develop a set of powerful grants and tax incentives and invest in a robust public charging network.

“While only a handful of EVs were on sale in 2011, there are now more than 100 models available.” Poppy Welch, head of Go Ultra Low

“The latest BVRLA data shows that the fleet sector continues to lead the charge towards zero emission motoring, with battery electric vehicles responsible for 21% of company car registrations in the three months to October 2020.”

With so much uncertainty surrounding the impact of EU Exit, coronavirus and the economic downturn, Keaney says that the Government must do everything it can to support the vehicle buyers that underpin the UK’s new car market.

“With the next Budget just weeks away, the Chancellor must continue to ring-fence the long-term grants and tax incentives that make electric vehicles affordable,” he said.

“He must also resist the urge to pile more motoring tax increases on fleets and drivers that have yet to make the transition to zero emission motoring.

“Many of these businesses and individuals are struggling financially and can’t yet find an electric vehicle that meets their needs or budget.”

More than 100 plug-in car models are now available to UK buyers, and manufacturers are scheduled to bring more than 35 to market in 2021 – more than the number of either petrol or diesel new models planned for the year.

Poppy Welch, head of Go Ultra Low, believes that in the context of the new car market, 2020 will be remembered as the breakthrough year for EVs.

“After a ninth successive year of growth in EV registrations, we’ve now seen market share rise to 10.7%,” she said.

“This has been made possible, in large part, by the Government’s ongoing support and long-term vision, combined with the automotive industry’s commitment to developing a wide range of zero-emissions vehicles that are clearly convincing the public with their performance, financial and environmental credentials.

“While only a handful of EVs were on sale in 2011, there are now more than 100 models available.”

When will the market get ‘back on its feet?

Ashley Barnett, head of consultancy at Lex Autolease, said that the 29% year-on-year drop really “hammers home” just how challenging the coronavirus pandemic has been for the motor industry.

“The market will take some time to get back on its feet,” he said. “How long that is remains to be seen.”

He added: “The growth in EVs is comforting but ultimately is from an extremely low base – only 6.6% of vehicles on the roads are EVs (including PHEVs).

“All eyes will be firmly on the spring Budget and the rumoured plans for a road pricing scheme which may go some way to recoup lost tax revenue when EVs begin to overtake conventional ICE models.

“The Chancellor has an opportunity to reassure would-be EV drivers that fiscal incentives will remain on the table and incentivise them to take the first step into alternatively-fuelled vehicles.”

Jon Lawes, managing director of Hitachi Capital Vehicle Solutions, expects economic uncertainties to continue into the first quarter of 2021, while the pandemic dampens consumer confidence.

However, he said: “The UK’s long negotiated tariff-free trade agreement with the EU should provide a welcome boost for the motor industry to lay the foundations to support a recovery in the sector.

“Similarly, the positive trend in EV uptake demonstrates that the transition to electric will gather momentum in the months ahead heightened by the wide range of new EV models coming to market in 2021 and growing consumer demand.”

By Graham Hill thanks to Fleet News & SMMT

Share My Blogs With Others:These icons link to social bookmarking sites where readers can share and discover new web pages.

SUV Sales Across Europe Drop For First Time In 6 Years

The growth in demand for SUVs across Europe has slowed for the first time in six years as smaller, electrified models start to claw back sales.

Between January 2016 and January 2020, the market share of SUVs grew significantly – from 25% to 40%.

For the majority of the year, the market share of SUVs remained stable – between 40% to 41%. However, their registrations fell by 13% in November, and 21% YTD when compared to 2019.

Felipe Munoz, global analyst at JATO Dynamics, said: “The market has benefitted hugely from a wider SUV offering provided this year. But with the impact of Covid-19 still in full force, demand is no longer growing in parallel to new product launches, nor at such a fast pace.”

Conversely, B and C cars experienced declines below the overall average, in fact, their market share increased in November due to new arrivals and a more competitive electrified offering.

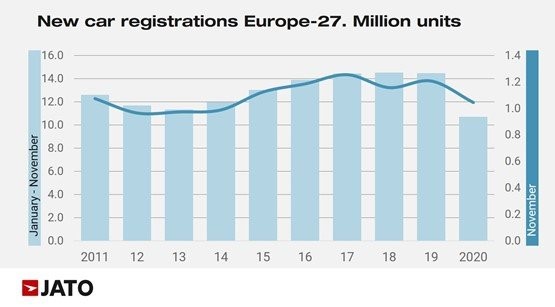

Overall, Europe registered 1,045,129 new cars – 13% less than for the same period in 2019. November 2020 has recorded the lowest volume since 2014, when just 989,500 units were registered.

Year-to-date figures continue to point to a downward trend, with YTD volume dropping by 26%. European consumers registered 10.71 million units between January and November – the lowest YTD figures so far this century.

Munoz added: “The global pandemic and its impact on mobility has been extremely painful for the automotive industry, indeed more painful than any other economic crisis that has hit Europe over the last two decades.”

The overall ranking by models in November confirms that the Volkswagen Golf (pictured) kept its position as the most popular car in Europe. The hatchback registered 24,800 units in November – just short of 255,000 units since January.

Only two SUVs made it into the top 10 – the Peugeot 2008, followed by the Renault Captur. Further down the ranking, Ford Puma, Volvo XC40, Audi A3, Renault Zoe, Volkswagen ID3, Kia Niro, Mercedes GLA, Skoda Kamiq, Jeep Compass, Mercedes GLB, Nissan Juke, Audi Q3 Sportback, Kia Xceed, Suzuki Ignis, and BMW 2-Series, all posted healthy results.

By Graham Hill thanks to Fleet News

Share My Blogs With Others:These icons link to social bookmarking sites where readers can share and discover new web pages.

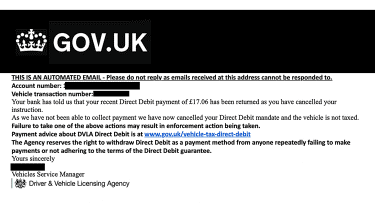

The following is just one of a series of emails being sent to drivers by scammers in order to defraud them.

The Driver and Vehicle Licensing Agency (DVLA) has seen a six-fold increase in scam reports. Between July and September 2020, the DVLA received 603 per cent more reports of fraudulent emails, texts and phone calls than it did in the same period last year.

There were 3,807 reports of email scams alone – up 531 per cent from the 603 reported in the three months to September 2019. Reports of fraudulent texts, though, decreased from a 653 between July and September 2019 to 510 in the same period this year.

These fraudulent messages can ask drivers to verify their driving licence details, offer vehicle tax refunds, or highlight a failed vehicle tax payment and ask for bank details.

The DVLA has now released images of some of the most commonly reported fraudulent emails, allowing drivers to familiarise themselves with them and avoid them.

How to protect yourself against the scammers

Drivers are reminded that the only place they can access official information on the DVLA and its services is the GOV.UK website. The DVLA never asks for bank details over email and never sends text messages about vehicle tax refunds.

The DVLA also tells motorists to never share driving licence images and vehicle documents online, never share bank details or personal data online, avoid websites offering to connect to DVLA’s contact centre and only use GOV.UK when looking for DVLA contact details.

Suspicious emails and texts should be reported to the National Cyber Security Centre. You can also forward a questionable text message to your mobile network provider on 7726. Furthermore, anyone who thinks they may have been a victim of fraud should immediately contact the police via Action Fraud.

Phil Morgan, head of fraud policy investigation at the DVLA, said: “These new figures demonstrate that scammers are becoming more persistent in their efforts to target motorists.

“These more recent scams may at first seem legitimate, however they are designed to trick motorists into providing their personal details. We never ask for bank or credit card details via text message or email, so if you receive something like this, it’s a scam.” By Graham Hill thanks to AutoExpress

Share My Blogs With Others:These icons link to social bookmarking sites where readers can share and discover new web pages.

The Government is being urged to work with the fleet sector to ensure any changes to motoring taxation are carried out in a timely, effective and proportionate way.

Reports suggested that the Government was considering reviving road pricing plans to counter lost tax revenues from the increasing adoption of electric vehicles (EVs).

The fleet sector has already shown it is receptive to road pricing as a replacement to other road and fuel duties. Fleet News has been calling for the Government to launch a feasibility study since its Fleet Industry Manifesto report in 2015.

The National Infrastructure Strategy, launched to coincide with the Spending Review, emphasised the need for motoring tax revenues to ‘keep pace’ with the uptake of EVs. It did not, however, mention road pricing as a potential alternative to the current regime.

Gerry Keaney, chief executive of the British Vehicle Rental and Leasing Association (BVRLA) says any changes need to be fair to the fleet industry.

He recognises that the Government’s future motoring tax strategy must strike a “fine balance” in maintaining vital revenues and encouraging people into newer and cleaner vehicles.

But he stressed: “The Government must avoid placing a crushing tax burden on businesses and individuals that are unable to upgrade their cars, vans or trucks and are already struggling to cope with the economic implications of Covid-19 pandemic and EU exit.”

The Government has already spent £280 billion to help support the economy through the pandemic and will spend a further £55bn next year to support the recovery.

“We will very soon need a system that can levy tax on both conventionally fuelled and battery electric vehicles fairly,” Nicholas Lyes, RAC

In total, taxes on UK motoring, including vehicle excise duty (VED), fuel duties and VAT, raise around £40bn per year or 7% of total revenue to the Exchequer. Of this, benefit-in-kind (BIK) tax payments, covering the provision of company cars, raise close to £1.8bn.

Darren Handley, head of infrastructure grants at the Office for Low Emission Vehicles (OLEV), told attendees at Virtual Fleet and Mobility Live that, while the question of future motoring taxation is one for the Treasury, it should not necessarily follow that lost fossil fuel revenues will be recouped from EV drivers.

He said: “If you look at a parallel with something like health and smoking, any reduction in tax (take) from (a reducing number of) smokers isn’t regained by taxing somebody who is healthy.”

Covid-19 impact on tax revenues

In Budget 2020, the Treasury outlined expected tax receipts from fuel duty each year up to 2024/25. It expected to collect £27.5bn this tax year, a £200m decline on £27.7bn in 2019/20. But, then it was predicted to increase to £28.1bn the following year (2021/22), before reaching £30.5bn in 2022/23, £31.2bn in 2023/24 and £31.7bn in 2024/25.

VED receipts are expected to fall by £100 million to £7bn in 2021/22, before increasing by £200m each year for the next three years, reaching £7.6bn in 2024/25.

Revenues, however, have already been impacted by Covid-19, with lockdown restrictions reducing fuel duty by £2.4bn in April and May compared with the same time last year.

Nicholas Lyes, RAC head of roads policy, said: “While not paying car tax is clearly an incentive to go fully electric at the moment, we will very soon need a system that can levy tax on both conventionally fuelled and battery electric vehicles fairly.

“If this isn’t addressed, we risk finding ourselves in a situation where petrol and diesel drivers continue to pay all the tax for using the roads which is unsustainable.”

Four-in-10 drivers believe that some form of ‘pay-per mile’ system would be fairer than the current system of fuel duty, says the RAC, while half (49%) agree that the more someone drives, the more they should pay in tax.

Insurance and Mobility Solutions (IMS), which is part of Trak Global Group, has successfully piloted road pricing projects in several US states.

Dr Ben Miners, chief innovation officer for IMS, explained: “Road user charging (RUC) and electronic toll collection (ETC) are both important solutions to fairly generate revenue from road users.”

ETC focuses on specific concessions or fixed points with a roadside/infrastructure approach, whereas RUC focuses on the broader transportation network with an infrastructure-free, wireless infrastructure, process.

Miners said: “The additional flexibility of RUC enables new virtual tolls to be introduced and transform any road segment or fixed asset into a ‘tolled’ road, which eliminates lengthy construction times and shortens time-to-market.” By Graham Hill thanks to Fleet News

Share My Blogs With Others:These icons link to social bookmarking sites where readers can share and discover new web pages.

Cash-takers are returning to company car schemes in “noticeable” numbers thanks to the attractiveness of electric vehicles (EVs), reports Arval UK.

The Government introduced a new zero percentage benefit-in-kind (BIK) tax rate for pure EVs from April this year, and the leasing company says that plug-in company cars are now really gaining traction in the market.

Shaun Sadlier, head of consulting at Arval UK, explained: “Many cash takers liked their company car but didn’t like paying what they perceived as high benefit-in-kind and that was why they opted-out.

“Now, with low benefit-in-kind in place for EVs for at least five years, many more are now returning to company car schemes.”

Arval predicted that this would start to happen some time ago, but Sadlier said: “It’s now becoming noticeable In several of the major fleets with which we work.

“It’s a welcome development that will feed demand for zero-emission vehicles and lead to wider, faster adoption.”

New BIK rates are driving the choice in zero emission vehicles, but Arval believes that there are also a range of other factors in play.

“If you talk to fleet managers and their drivers, there’s a lot of enthusiasm around the vehicles themselves,” continued Sadlier. “We are beyond the early adopter phase and heading into mass-acceptance.

“All it takes is a couple of EVs on a fleet to disprove the reservations some people hold about these vehicles.

“They can see that misgivings such as range anxiety are actually of limited importance for the vast number of journeys that are made.”

Arval UK recently updated its own company car scheme to increase adoption of EVs and the move paid off with almost two thirds of its company car drivers making the switch so far.

Sadlier said: “All of our consultants and many of our sales team have switched to EVs.

“They act as ambassadors for the technology, developing personal experience to share with customers, friends and family – as more people drive EVs, consumer confidence will increase.

“Coupled with the growing number of different models that are available, plus the recent 2030 announcement, it’s not an exaggeration to say that we can all play our part in a zero-emission future and choosing an EV is a step in that direction.” By Graham Hill thanks to Fleet News

Share My Blogs With Others:These icons link to social bookmarking sites where readers can share and discover new web pages.

The amount fleet operators and consumers with PCH are paying in end-of contract excess mileage charges for cars has risen significantly for the second consecutive year.

This year’s FN50 (top 50 leasing companies) research has found the average charge for defleeted company cars is £449, 19% higher than last year, which itself was 17% higher than in 2018. The 2018 figure was a record low of £324. The figures are similar if not slightly higher for consumers.

There remains a huge disparity in the size of the average charges reported by individual leasing companies and these range from as little as £20 to £900. The extremes highlighted in last year’s FN50 were £28 and £1,182.

Of the respondents to this part of the FN50 research, 38% of leasing companies had charges above the average amount, with 63% of those at £700 or above.

Of those with charges below the average, 15% were £100 or less.

The average proportion of cars subject to excess mileage charges has fallen one percentage point from last year to a record low 18%. Over the longer term, this proportion is significantly lower than the 2005 figure of 32%.

There is also a large disparity between leasing companies in the proportion of cars subject to excess mileage charges.

These ranged from as low as 0.5% to as high as 61%. There was a £350 difference in the size of the actual average charges these two companies billed: £440 and £790 respectively.

Just more than one-quarter (28%) said the proportion of cars returned which were subject to excess mileage charges was 10% or lower, while 24% said their average figure was about 25%.

Meanwhile, van operators fared much better with excess mileage charges. The average charge for vans fell £2 from 2019’s figure to £482, which points to a year of relative calm after the previous year’s 40% increase.

Those leasing companies with above-average charges for cars accounted for 67% of the companies with above average charges for vans.

As with cars, there is a huge disparity in the average charges reported by individual leasing companies, ranging from £55 to £900.

Of the leasing companies which supplied this information, 42% had charges above the average amount, with 16% at £750 or above. Of the companies below the average, 50% were £250 or less.

The average proportion of vans which were subject to excess mileage charge has remained steady over the past three years.

This year it was 19%, two percentage points below last year’s figure and one percentage point lower than 2018. Two-in-five (38%) respondents reported being at or above the average figure.

As with cars, there was a large disparity between the proportions reported by individual leasing companies. The lowest figure was 2% and the highest 85%.

Overall, 28% of respondents said their average proportion of vans which were subject to the charges was 10% or lower, while 12% were above 50%.

Like last year, there does not seem to be a common factor to determine why the excess mileage trends have either increased in the case of cars or slightly decreased for vans.

There is no consistent patterns in the duration of average replacement cycles operated by the leasing companies with the highest charges, or whether vehicles were being returned early, on time or late at the end of their terms.

Another unknown is the effect the Covid-19 pandemic had on this year’s figures. In July, a Fleet News survey of 150 fleet decision-makers found almost 61% expected to see average mileages of their company car fleet fall.

More than half (57%) of respondents said the majority of company cars they operate were not being driven for work, while 43% said less than one-third of the vehicles on their company car fleet were being driven for work.

This would suggest vehicles could either have been returned with lower than expected mileages as business travel reduced, although many fleets extended their vehicle contracts during the pandemic. Other vehicles could be likely to incur increased charges due to an increased workload.

LOCKDOWN HELP

During lockdown, leasing companies worked to mitigate the impact on mileage charges.

For example, Miguel Cabaça, managing director of Arval UK, says: “Arval will be as understanding as possible in these difficult times.

“We will be having individual discussions and be offering proactive solutions client-by-client.”

Leaseplan said customers’ individual mileage allowances would continue to roll on, on a pro rata basis, if leasing agreements were extended.

This year’s FN50 should provide a clearer picture of the impact of the pandemic on business mileage and how fleet decision-makers have managed their vehicles during the crisis, as more leases expire and vehicles are returned to their leasing providers.

Previous FN50 reports have suggested that when end-of-contract charges are falling, it is most likely through contract hire companies keeping track of mileage and discussing higher mileage than agreed with customers mid-term, and allowing flexibility to increase monthly rental rates to compensate so there would not be a large excess mileage bill at the end of the fleet lifecycle.

These are among the measures introduced by Free2Move as it has focused on reducing excess mileage charges for its customers.

“We have taken two very decisive moves in this area in recent years, taking account of prior dissatisfaction in the market at the level of these charges,” said Mark Pickles, managing director of Free2Move.

“Pence-per-mile rates for excess mileage have been reduced to take account of the ‘real’ impact on residual values, rather than to be used as a ‘penalty’ or profit opportunity – treating our customers fairly is a core principle.

“We also have a large number of our fleet fitted with onboard tele-matics, using our own Free2Move Connect Fleet system, to be able to monitor the mileage on a real-time basis.”

Where Free2Move sees mileage is starting to trend above the contract-agreed figure, it calls its customers to find out if they are aware of this, if it is a trend that is likely to continue or is a seasonal aberration, or if they would like to amend their contract to avoid any end-of-contract penalties.

Pickles added: “Most customers, faced with this up-to-date and reliable information, elect to increase their monthly lease payment slightly to cover the extra mileage and avoid a nasty surprise at the end.

“In the same way that we are used to our gas and electricity bills being adjusted to take account of higher usage rather than building up a deficit on our home energy account, Free2Move is able to neutralise this impact and give the customer a choice of how to deal with a change in usage.

“By utilising the telematics data, we can avoid false alarms, see patterns emerging and give fleet managers the choice of how they wish to manage the change.”

Pickles adds that pooled mileage arrange-ments give its larger customers more flexibility and reduce the need to swap cars or vans between users to manage mileage, resulting in fewer excess mileage charges and less intervention on the part of the customer.

The average proportion of trucks which attracted excess mileage charges also increased year-on-year, this time by three percentage points to 10% compared with 2019.

The average charge was £600 – 50% less than in last year’s FN50 report, while the disparity in the proportion of trucks subject to excess mileage charges reported by individual leasing companies was much smaller than with cars or vans, ranging from 9% to 12%. By Graham Hill thanks to Fleet News

Share My Blogs With Others:These icons link to social bookmarking sites where readers can share and discover new web pages.

Residual values could fall by 10% over the next year as the economic effects of a recession and high unemployment bite.

The prediction is included in the BVRLA’s latest Leasing Outlook report, which warns the vehicle leasing industry is braced for yet more challenges as “the most turbulent year imaginable” comes to an end.

The report says the sector remains agile but is also seeking clarity around the impact of Brexit, the Covid-19 pandemic and the transition to zero-emission motoring.

BVRLA members expect battery electric vehicles to hit 6% of the total lease car fleet by the middle of next year, with plug-in hybrids hitting 9%.

Petrol’s market share will begin to plateau at around 38%, with diesel slipping under 50% for the first time at 46%.

Andrew Mee, head of forecast UK at Cap HPI, told the report: “On average, used car values are now around 7% higher than they were a year ago and we consider this unsustainable.

“As we move through Q4, we expect that the strength in the used market may start to slowly ebb away, as pent-up demand is satisfied and the typical pattern of falling values in the latter months of the year could be re-established.

“A fall of 10% over the next year looks reasonable.

“It is broadly similar to 2019 and is nowhere near as bad as we saw in 2008.”

The report says there will be an improvement beyond 2021, but it will not be as rapid as it was in 2009, due to Covid having a much broader and more complex set of impacts on the economy and automotive market.

The three other broad themes covered by the report are:

Supply chains – leasing companies are looking forward to a rebound in demand for fleet vehicles as the economy recovers but are concerned about the potential for extended lead times and the reputational damage that could ensue.

Brexit – The type of EU-Exit we get will have a huge impact on business confidence, lead times, the cost of new vehicles and the ease with which they can be moved around the UK and Europe.

Liquidity – The financial and administrative burden of providing forbearance to those hit by the pandemic will last well into 2021 and there are signs that the supply of motor finance is also tightening.

By Graham Hill thanks to Fleet News

Share My Blogs With Others:These icons link to social bookmarking sites where readers can share and discover new web pages.

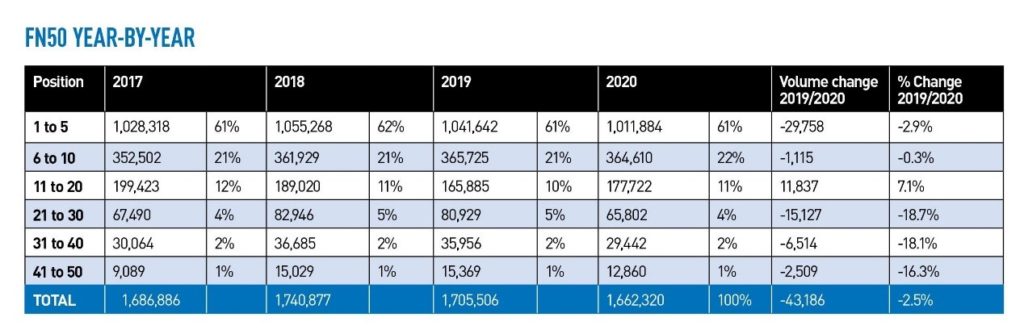

For the second consecutive year, the FN50 top 10 has, aside from some minor positional shuffling, remained the same: the same companies largely in the same places.

The two exceptions are Arval and LeasePlan switching places and an identical swap by Free2Move and Zenith.

Also occurring for the second consecutive year is a decline in total car and van volumes funded by the UK’s 50 biggest leasing companies. The 2.5% reversal, or 43,186 vehicles, is slightly higher than the previous year’s 2%/35,371, resulting in an FN50 funded fleet of 1,662,320 vehicles.

However, where last year the drop in vehicles was largely prompted by the exit of Mercedes-Benz Financial Services (now retail only) and Sandicliffe Motor Contracts (no longer funding), the year it is due to an industry-wide reduction in company cars.

This is a result of people opting for cash (the number of employees paying benefit-in-kind (BIK) tax on a car continues to fall – 90,000 have left a car scheme over the past five years) and, more recently, by the impact of Covid-19 on jobs, although the full shock of this impending economic crisis is still to be felt.

And, while opt-outs are often converted into personal leases, this hasn’t plugged the gap.

Consequently, the number of company cars in the FN50 has fallen year-on-year by 3.3%, or 41,080 units, while vans saw a negligible 0.5% dip of 2,106 vehicles.

It continues a three-year trend of vans taking a gradually increasing share of the total number of vehicles funded by the FN50: in 2017 they accounted for 24%; this year it’s 27%.

The FN50 data presents a slightly less sombre picture than the recent industry-wide figures released by the British Vehicle Rental and Leasing Association which showed a lease fleet decline of 3.6% year-on-year, at a little more than 2.53 million vehicles.

However, its survey revealed growth in the van fleet by 2.1%, which partially offset a heavier deficit in cars of 5.2%.

Swing towards PCH

Healthier performance by personal leasing Business contract hire bore the brunt of the losses, down 9.7%, while personal contract hire (PCH) enjoyed a healthier performance, up 5.7%. This is echoed by the FN50 members, where the larger organisations have been extending their penetration into the personal leasing sector in recent years.

The past couple of years have seen a definite swing towards PCH among the UK’s biggest leasing companies. In 2018, fleet leasing accounted for 87% of their car business; this year that has fallen to 80%. Almost a quarter of a million cars (244,194) are now PCH.

Often, manufacturer-owned leasing providers have a greater proportion of retail business due to the agreements sold via their franchised dealers, such as FCA’s Leasys at 69% and Renault’s RCI at 67%, while ALD, which powers white label finance for the likes of Kia and Ford, is also weighted towards private leasing. Santander Consumer Finance (the clue being in the name) is 82.5% private and Affinity Leasing, which specialises in corporate affinity schemes for employees, is 96% private.

With the likes of Zenith (ZenAuto) and Arval (Arval for Employees) stepping up their retail aspirations, and growth in salary sacrifice schemes (although not all leasing companies view these as private leasing because of the central agreement with the employer), plus bank-owned organisations such as Lex Autolease improving internal synergies, personal lines could tighten their grip on the FN50 numbers in the coming years.

“The market has been diversifying for many years now and personal leasing in its various forms has penetrated both the retail market and corporate sectors,” says Craig McNaughton, corporate director at the UK’s biggest fleet lender Lex Autolease.

However, a compelling counter-argument centres on the growing attractiveness of electric and plug-in hybrid cars due to the very low BIK tax rates over the next four years.

Some leasing companies are already reporting electric cars accounting for 30-40% of their order books.

McNaughton again: “The advent of 0% BIK for EVs and low BIK for ULEVs has seen movement back into company cars and salary sacrifice.”

He believes that traditional fleet funding methods will remain dominant, despite suggestions among some industry commentators that a growing need for flexibility will persuade companies to negotiate shorter terms and consider alternative funding arrangements.

“We have been part of subscription trials with partners and they do have potential in very specific circumstances, but the economic model for such services remains a challenge, as can be seen by the poor financial results that continue to be delivered by traditional vehicle rental companies,” he says.

“As such, changes to shorter leases and more flexible products are likely to remain small scale due to their relative expense with the market continuing to mainly fulfil demand for providing long-term leasing/funding solutions.”

Nevertheless, flexibility is a recurring theme during 2020 due to the uncertainties caused by Covid-19 and a surge in people working from home, reducing their dependence on the car.

Alphabet doesn’t see subscription services as a replacement for traditional funding, but it does recognise the need for increasing flexibility, according to chief commercial office Simon Carr.

“We expect to see a rise in demand for shorter term, adaptable leasing arrangements to bridge the gap between rental and longer-term leases as drivers’ roles and requirements change,” Carr says.

“Funding choices will become even more data-led and wholelife costs will play an even bigger part in fleet managers’ decisions as the total cost of mobility will be key to running a successful fleet in a time when travel has naturally reduced.”

Flexibility doesn’t just mean shorter terms, however. Salary sacrifice expert Tusker has responded to customers’ needs to “provide shorter and longer agreement options for employees to increase inclusion for lower earners and those on shorter employment contracts”, says CEO Paul Gilsham.

EVs stimulating growth

Meanwhile, Claire Evans, fleet consultancy director at Zenith, believes EVs are stimulating growth in all sectors of the market, from company cars to salary sacrifice to personal contracts.

“We are already seeing a trend into leased vehicles and away from ownership with the growth in electric vehicles and movement to subscription-based services based on monthly affordability,” Evans says.

“It has resulted in increases in salary sacrifice and personal contract hire cars, where EVs account for one-in-two and one-in-four orders placed this year, respectively. We expect to see this trend continue.”

As part of the FN50 survey, leasing companies provide data on the vehicles they manage on behalf of a fleet customer but don’t fund.

For cars, the numbers have risen, showing that the need by UK business for fleet management support is growing, as outsourcing of a function sometimes seen as non-core continues.

This year, the number of cars under fleet management has risen by 27,046 to 259,518; meanwhile, the number of vans has fallen slightly, from 62,808 to 62,129.

As a business essential tool, vans are much more likely to be an in-house responsibility, particularly if the company also runs trucks with their elevated legal and compliance requirements.

The rise in fleet management has helped many leasing companies to offset the reversals in fleet funding.

With three new entrants in 2020, 26 of the 47 returning FN50 companies saw their funded fleet fall compared with 2019, up from 19 companies last year.

By far, the biggest impact was felt by those left outside the top 20 (see table), where double-digit falls were commonplace.

Half of the top 10 are funding more vehicles than a year ago, with notable growth in cars and vans by Arval, lifting it by 6% to leapfrog LeasePlan into third place, and seventh-placed Hitachi Capital Vehicle Solutions, up 7% thanks to wins in both cars and vans.

Free2Move bumped Zenith from eighth after a 5% boost to its funded business, almost entirely cars with a 7,000-unit rise, while Zenith experienced a marginal 1% drop in funded business – although its van division was up year-on-year.

Zenith has also extended its penetration into the truck business with the acquisition in September of Cartwright Fleet Services, Cartwright Rentals and Cartwright Finance Sales from the administrators.

The move created one of the UK’s largest HGV and specialist fleets with more than 50,000 vehicles and one of the UK’s largest trailer rental fleets.

It also underlines how some of the UK’s top lenders are now multi-asset funders with a breadth of interests, from salary sacrifice, job need and perk cars to vans, trucks and trailers.

And some are starting to gow even further, with e-scooters/ e-bikes, car share and other forms of mobility services. By Graham Hill thanks to Fleet News

Share My Blogs With Others:These icons link to social bookmarking sites where readers can share and discover new web pages.